Editorial Note: We earn a commission from partner links at Forbes Advisor. Commissions do not affect the opinions or ratings of our editors.

Drivers are not pumping their brakes when it comes to approving the use of non-driving factors in car insurance price — other than sex — according to a new Forbes Advisor survey of 2,000 drivers who have car insurance.

Sex, credit, education and occupation are commonly used by car insurance companies when setting rates. The survey measured consumer views on these practices.

Here’s a look at what Americans think about factors that affect auto insurance rates and how they judge the cost of their own auto insurance.

Battles of the Sexes: Using Gender in Auto Insurance Rates

Contents

- 1 Battles of the Sexes: Using Gender in Auto Insurance Rates

- 2 Approval Nearly Doubles for Use of Credit in Car Insurance Quotes

- 3 Education: Twice as Many Drivers Now Say Include It

- 4 Over Half Say Occupation Should be a Factor in Car Insurance Quotes

- 5 2021 vs. 2022: More Drivers Say Their Car Insurance Rates are Fair

- 6 Monitoring Actual Driving? People Are Getting Comfy With It

- 7 Over a Quarter Think Other Drivers are Not Very Good or Terrible

- 8 Best Car Insurance Companies 2022

- 9 Survey Methodology

- 10 Do you get better insurance rates with good credit?

- 11 How does your gender factor into auto insurance rates?

- 12 What is a factor that increases costs of insurance premiums?

- 13 Qui sont les clients du Groupe Crédit Agricole ?

Most drivers surveyed do not favor car insurance companies using sex when calculating car insurance quotes, but results between females and males differ significantly. Read also : How Car Insurance Can Bring High Lemonade Stores.

The majority of drivers (62%) said that sex should not be a factor in car insurance quotes. Nearly three-quarters of women (72%) do not support it, compared to 41% of men.

However, women usually pay less for car insurance than men, according to a Forbes Advisor analysis of how age and gender affect car insurance premiums.

In your opinion, should auto insurance companies take a driver’s gender into account when it comes to pricing?

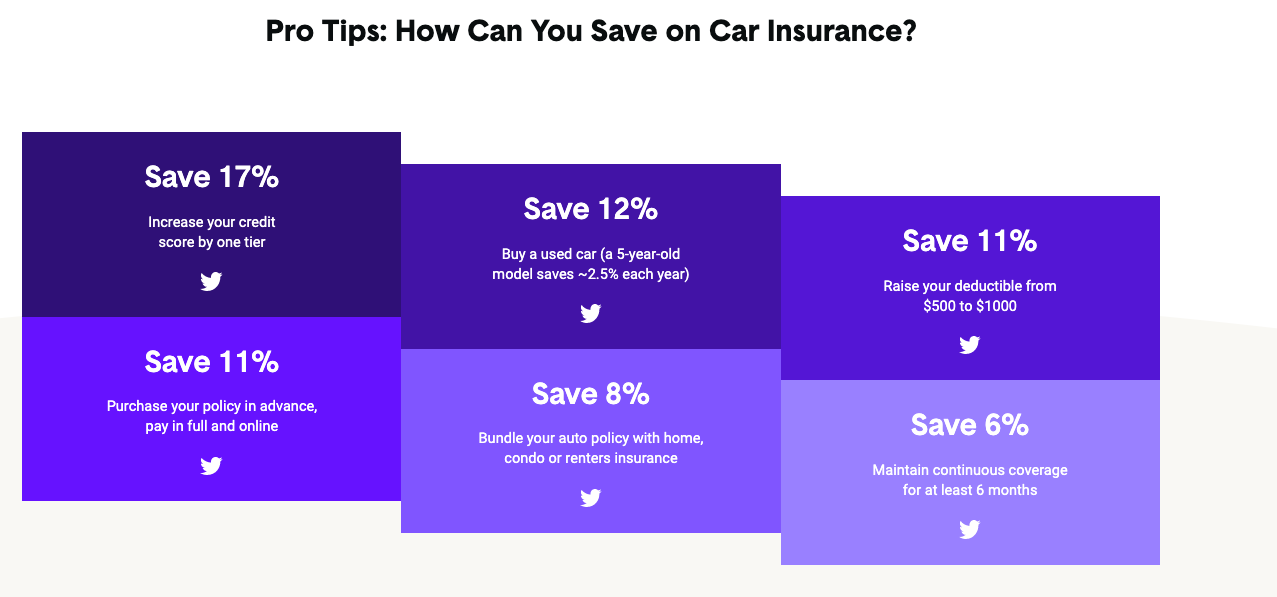

Approval Nearly Doubles for Use of Credit in Car Insurance Quotes

The use of credit by insurance companies as a factor in car insurance quotes is one of the more controversial pricing factors. Insurers say a person’s credit correlates with the likelihood that the person will take out insurance. Read also : 96% of American drivers do not understand their car insurance policies. Many insurers put a heavy burden on credit-based insurance scores when setting prices.

However, based on Forbes Advisor’s comparison of a survey from 2021 to this year, more people are warming up to the idea of credit as a factor in car insurance quotes:

More than a third (36%) of survey respondents did not think that a driver’s credit score should be used to determine auto insurance, compared to 69% last year. This is a 48% decrease in the number of people who disapprove of using credit scores on car insurance quotes.

To what extent do you agree or disagree with the following statement: “Auto insurance companies should take the driver’s credit score into account when it comes to pricing”?

Consumer advocacy groups and some lawmakers say using credit-based scores unfairly increases car insurance rates for certain demographics and is fundamentally discriminatory. See the article : Is State Farm overpriced?.

A Forbes Advisor analysis of car insurance rates in the 46 states that allow credit as a price factor found that drivers with bad credit experience an average rate increase of 76% compared to drivers with good credit. That translates to about $ 1,180 annually. California, Hawaii, Massachusetts and Michigan prohibit the use of credit in setting auto insurance premiums.

Related: How much is the car insurance premium due to bad credit?

Education: Twice as Many Drivers Now Say Include It

Drivers seem to accept the use of educational levels in car insurance quotes. When asked whether education should be considered, 46% supported the idea, which marked a 119% jump from last year, when only 21% supported it.

More than a quarter (28%) did not agree that the level of education should be considered, compared to 67% last year.

Insurers could include a level of education in car insurance quotes when they made a connection between a higher degree and less insurance claims. And many auto insurance companies give discounts on education, rewarding drivers who have earned a bachelor’s or master’s degree or a Ph.D.

To what extent do you agree or disagree with the following statement: “Auto insurance companies should take the driver’s level of education into account when it comes to pricing”?

Over Half Say Occupation Should be a Factor in Car Insurance Quotes

More than half of drivers (58%) think it’s a good idea to use car insurance prices. In 2021, only 36% of drivers thought that someone’s work should be considered in a rate for car insurance.

Only 16% of drivers did not believe that a person’s occupation should affect fares. That’s a big drop from 2021, when 44% said someone’s work shouldn’t be a factor in car insurance quotes.

Like other pricing factors that are not about actual driving, some insurers give discounts for certain occupations. For example, lawyers, doctors, and educators may earn lower rates.

To what extent do you agree or disagree with the following statement: “Auto insurance companies should take the driver’s occupation into account when it comes to pricing”?

2021 vs. 2022: More Drivers Say Their Car Insurance Rates are Fair

Despite a lack of consensus on using non-driving factors in car insurance rates, most drivers feel that their car insurance rates are fair or do not have strong feelings about them. The survey found that 58% of respondents think their car insurance rates are “fair” or “very fair”, compared to 48% last year.

The findings come even as rising medical costs and increasingly expensive car repairs have led to steady rates over the past several years.

Thinking about how much you are currently paying for auto insurance, do you believe you are paying a fair or unfair rate?

Monitoring Actual Driving? People Are Getting Comfy With It

For people who are very safe drivers, buying car insurance that focuses primarily on actual driving habits may be worth considering, and more motorists are warming up to the idea.

Use-based auto insurance, which uses actual driving data in rates, could reduce insurance companies’ reliance on non-driving pricing factors such as credit scores, employment and education. Using telematics, these insurance programs monitor and record actual driving, including speed, braking, and cornering.

More than half (64%) of survey respondents said they would be “very comfortable” or “somewhat comfortable” with their driving closely monitored if it could lead to lower car insurance rates. Last year only about half (51%) were comfortable with it.

Would you be comfortable allowing a car insurance company to closely monitor your driving (e.g. with a piece of equipment installed in your car) if it allowed you to receive lower insurance rates for good driving?

Over a Quarter Think Other Drivers are Not Very Good or Terrible

There is no shortage of high-tech telematics programs that can estimate how safe a driver is driving, but that doesn’t stop people from making their own estimates. Only 12% describe their co-drivers as “excellent”, and 28% consider them “terrible” or “not very good”.

How would you describe most other people as drivers?

Best Car Insurance Companies 2022

With so many choices for car insurance companies, it can be difficult to know where to start to find the right car insurance. We’ve rated insurers to find the best car insurance companies, so you don’t have to.

Survey Methodology

This online survey of 2,000 U.S. drivers who own a car and have car insurance was commissioned by Forbes Advisor and conducted by market research firm OnePoll, in accordance with the Market Research Society’s code of conduct. Data were collected 20-21 May 2022. The margin of error is +/- 2.2 points with 95% confidence. This survey was overseen by the OnePoll research team, which is a member of the MRS and has corporate membership with the American Association for Public Opinion Research (AAPOR). For a complete survey methodology, including geographic and demographic sample sizes, contact pr@forberadvisor.com.

BforBanko. BforBank is the 100% online bank of Groupe Crédit Agricole.

Do you get better insurance rates with good credit?

Under the III, if you have a high credit-based insurance score, an excellent driving history, and zero claims on your record, you will usually qualify for lower rates. This score is just one of many factors used to calculate your prize.

How does your gender factor into auto insurance rates?

Gender: Women can sometimes pay less for car insurance than men, according to the Insurance Information Institute, because they statistically tend to be involved in fewer and fewer serious accidents than men. Age: Age has a significant impact on fares, with teen drivers generally paying the highest premiums.

Does sex affect your car insurance rate? When it comes to buying car insurance, age and gender can affect rates. Women tend to pay less for car insurance than men. And it’s no surprise that young drivers pay the most. Age correlates with driving experience and the risk of getting into a car accident.

What is the gender rule in insurance?

Insurance rule. Determines the policy by which a parent covers offspring. Typically, parent policy is primary, providing dependent children coverage before considering any other possible coverage.

Does gender play a role in insurance?

Your gender can affect what you pay for car insurance, but not as much as other factors. The impact is most pronounced among the youngest drivers and varies by state. Some states do not allow the use of sex in calculating premiums at all.

Why do insurance companies ask for gender?

This is because research has shown men and women tend to have different driving styles and present different risks to the insurer. Younger men usually pay higher rates because they tend to be much riskier to insure. To be responsible for this risk, candidates must identify their gender when purchasing car insurance.

Does being male or female affect insurance?

For the most part, men and women pay about the same amount for car insurance. For typical adult drivers, we found only a slight difference in the cost of insurance between men and women. We found a price difference of less than 1% between men and women in their 30s.

Why does gender play a role in car insurance?

Most states allow sex as an assessment factor and insurers use sex because statistics show that crashes and claims are different for the different sexes. Younger and older males tend to have more accidents and thus pay higher rates.

Which gender plays more for car insurance?

Men pay significantly more for car insurance than women in their teens, while women pay slightly higher premiums in later years. On average, we found that men pay $ 720 a year for car insurance, while women pay $ 739 a year.

Why does gender matter in car insurance?

As drivers get older, female drivers are once again starting to pay less. One of the reasons men tend to pay more than women for car insurance is because men are more risky to insure.

Does car insurance change based on gender?

Changing your gender marker may or may not affect your car insurance rates. Insurers use many rating factors when determining your auto insurance premium. Some drivers may experience an increase after changing their sex marker, while others may enjoy a high-quality decrease, according to the NCTE.

Which gender pays the most for car insurance?

Women on average pay more than men for car insurance, despite fewer accidents, a study finds. Women can pay up to 7.6% more than men for car insurance, depending on their age and location, research by The Zebra finds.

Does car insurance vary based on gender?

States that do not allow auto-insurance rates based on gender. Not all states allow insurers to set rates based on gender. California, Hawaii, Massachusetts, Michigan, Montana, North Carolina and Pennsylvania all have statewide bans on using sex as a factor in car insurance rates.

Is male insurance higher than female?

Although men paid more in 2019, data from 2018 showed that women paid marginally higher premiums. For drivers over the age of 25, the difference between car insurance for men and women is largely insignificant until drivers reach the age of 60. Beyond that, fares for male drivers tend to be a bit more expensive.

Do single males pay more than married females for car insurance?

According to the study, there may be a significant difference between what a married person and a single person of the same age will pay for their car insurance premiums. On average, a single, 20-year-old man will pay 24 percent more for car insurance than his married counterpart.

Common reasons for high car insurance costs include your driving record, age, coverage options, where you live, the car you are driving, your credit history or not using discounts. The average car insurance premium has also become more expensive as it has increased by more than 50% in the past 10 years.

What factors affect insurance premiums? Some of the factors that can affect your auto insurance are your car, your driving habits, demographics, and the coverage, limits, and deductions you choose. These factors can include things like your age, anti-theft features in your car, and your driving record.

There are a few things that are beyond your control, but could still affect your premium, including: rising repair costs, an increase in distracted drivers on the road, more drivers on the road, higher speed limits in your geographic area, and an increase in uninsured drivers .

Factors influencing health insurance premiums

- Age – This is one of the critical factors that influence the overdose. …

- Past Medical History -…

- Occupation -…

- Policy Duration – …

- Body Mass Index (BMI): …

- Smoking Habits -…

- Geographic location: …

- The Type of Plan You Choose:

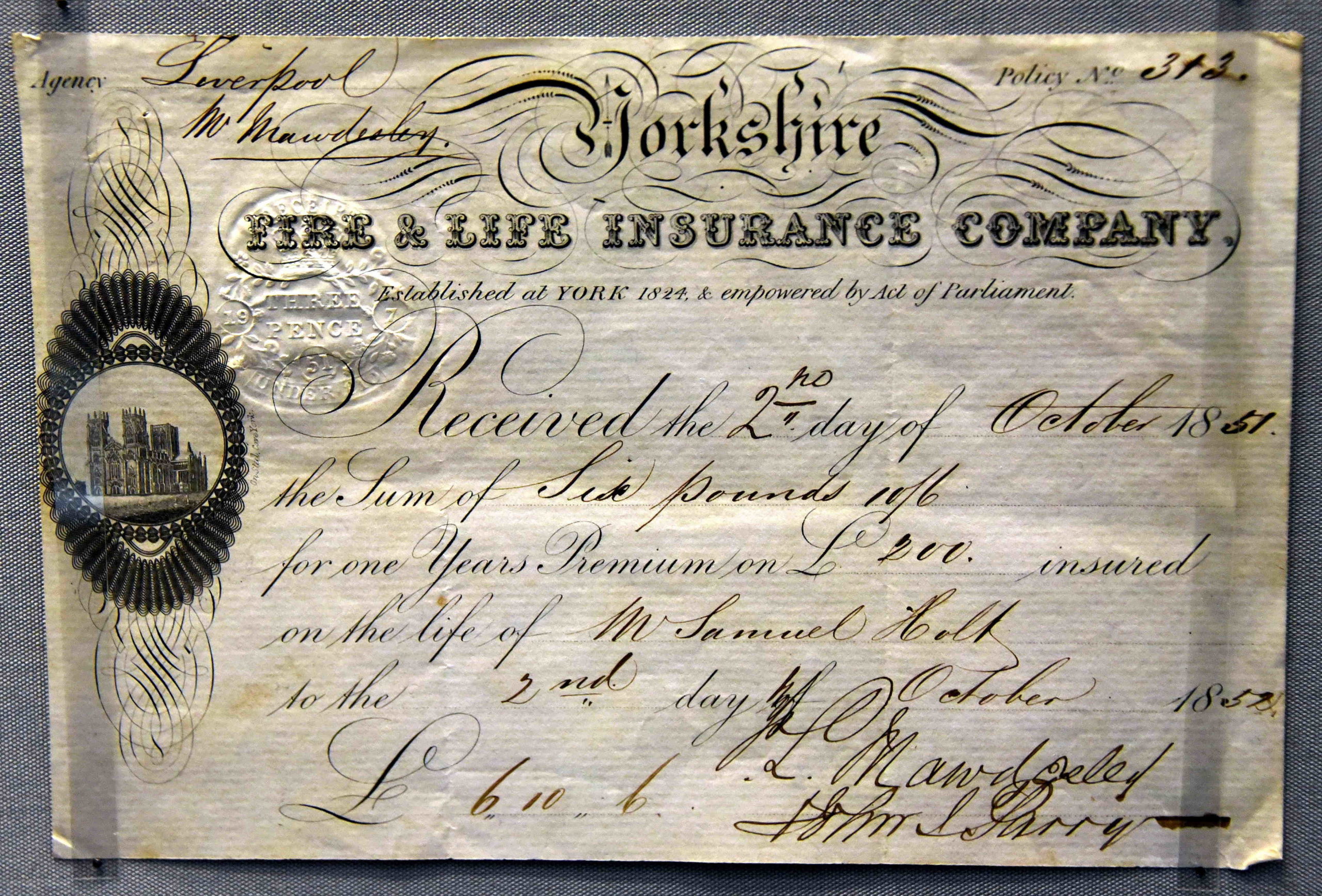

Climbing – also sometimes called climbing – is the amount by which your monthly premium will increase on a certain date. This can be a fixed amount like R100, or a percentage like 5%. Example: You pay R250 per month for R750,000 life insurance. Your prize increases by 5%, so the prize increases by R12.

Under the now-approved proposal by the Ministry of Road Transport, third-party car insurance premiums will rise to 21%, making it more expensive than ever to insure your car or durations. Insurance premiums have not been reviewed for two years, since the onset of the COVID-19 pandemic.

Qui sont les clients du Groupe Crédit Agricole ?

We put ourselves at the service of all, the most modest and wealthy households, the local professionals as well as the big international companies.

Are you Crédit Agricole’s customers? Key figures from the Crédit Agricole Regional Savings Banks

- 24.4 million customers.

- 1st bancassurer.

- 1ère bank of enterprises, with 1 enterprise on 3.

- 1st partner of public authorities.

- 1st real estate network.

- 1st farmers’ bank, with almost 9 out of 10 farmers.

Qui fait partie du Groupe Crédit Agricole ?

Crédit Agricole Assurances includes all the insurance activities of Crédit Agricole S.A., in France and abroad: Predica, Pacifica, Crédit Agricole Creditor Insurance, as well as the subsidiaries La Médicale and Spirica.

Quelles sont les banques du Groupe Crédit Agricole ?

| Agricultural credit | |

|---|---|

| Crédit agricole logo. | |

| Associates | 10 million |

| Activity | Banking and Insurance |

| Subsidiaries | LCL, CIB agricultural credit, Caceis, Cariparma, Amundi, Indosuez, Agricultural insurance credit, BforBank, Consumer finance agricultural credit, Uni-media, Square Habitat, Nexecur. |

Qui détient le Crédit Lyonnais ?

LCL is part of the Groupe Crédit Agricole, which has solid or cross-capital structures with liquidity and effective efficiency. Crédit Agricole is the 10th largest bank in the world by the size of its balance sheet.