Beyond inflation: Why car insurance rates are expected to rise in 2023

A shortage of auto technicians could affect car insurance premiums, according to The General.

Many Americans saw their car insurance premiums rise in 2022, and some studies project that the trend will continue into 2023.

The predicted increase in auto insurance costs has a variety of potential causes. These include ongoing supply chain issues across the auto industry, an increase in demand for skilled auto repair workers, fuel price volatility, and more, according to multiple studies.

“New vehicle and parts shortages, waves of retiring mechanics, and more dangerous roads are changing the auto insurance landscape for insurers and for you—the driver,” General Insurance said in a recent study.

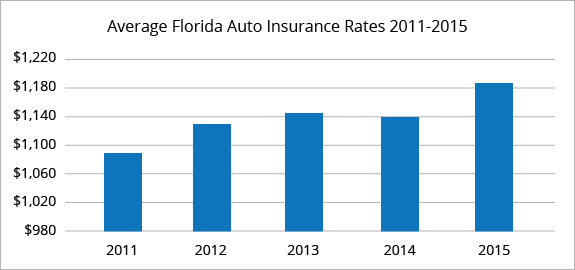

The average cost of auto insurance increased 9% to $1,777 per year in 2022, according to a recent report by Insurify. And it expects the rate to rise another 7% to $1,895 in 2023.

If you’re interested in saving money on your car insurance, consider switching insurance companies to get a lower monthly rate. Visit Credible to search and find your personalized award without affecting your credit score.

AUTO INSURANCE SPENDINGS ARE INCREASING: LEARN HOW DRIVERS ARE SAVING MONEY

Auto shop workforce trends may impact insurance costs

Contents

- 1 Auto shop workforce trends may impact insurance costs

- 2 Gas price uncertainty can linger in 2023

- 3 Can insurance raise your rate for no reason?

- 4 Is inflation causing car insurance to go up?

- 5 Why do insurance rates keep increasing?

- 6 Can I freeze my car insurance?

The auto repair industry could soon face a major labor shortage as veteran workers retire and the auto industry becomes more technology-oriented, which could affect the cost of car insurance. See the article : Car insurance for 2022 is on the rise and forecast.

By 2024, the automotive and transportation industry may need to fill around 642,000 technical jobs, according to a 2020 projection by TechForce.

“Dealerships and lobby groups have partnered with schools and non-profit organizations in recent years to train the next generation of automotive technicians,” The General said in its study. “Their jobs have become more and more technologically advanced as cars are loaded with more computer parts.”

The report added, “The costly dilemma for motorists is anticipated to continue for at least the foreseeable future. The Bureau of Labor Statistics predicts that the number of automotive technicians employed in the United States will remain virtually unchanged through the end of the decade.”

If you want to reduce your car expenses, there are ways to reduce your monthly car insurance payments, such as switching providers. You can visit Credible to compare multiple providers and see if one is right for you.

MORE CONSUMERS BUYING NEW AUTO INSURANCE TO SAVE MONEY: J.D. POWER REPORT

Gas price uncertainty can linger in 2023

After gasoline prices across the country hit record highs in 2022, Americans may see some relief in car spending. The annual national average gas price in 2023 is expected to drop nearly 50 cents per gallon from the 2022 price to $3. On the same subject : Why Texans’ car insurance rates are rising.49, according to GasBuddy’s 2023 Fuel Outlook.

But the organization notes that ongoing issues, from the war between Russia and Ukraine to global economic uncertainty, could prevent the expected drop in prices. GasBuddy predicts that a national average of $4 per gallon could be achievable before and during the summer season.

The national average for a gallon of gasoline has increased five cents to $3.32 since the week ended Jan. 15, according to AAA reports.

“Gasoline demand is generally weak at this time of year,” AAA spokesman Andrew Gross said in a statement. “And it probably won’t start to increase until spring break approaches. So the main driver in this latest increase is the higher cost of oil, which is more than half of what you pay at the pump.”

If you’re looking to lower your monthly car costs, consider switching providers. You can visit Credible to get your custom rate in minutes without lowering your credit score.

Have a finance-related question but don’t know who to ask? Email Credible Money Expert at moneyexpert@credible.com and your question may be answered by Credible in our Money Expert column.

Can insurance raise your rate for no reason?

Insurance companies take factors beyond your car and personal driving habits into account when determining your rate. For example, the following factors can cause your insurance bill to go up for no apparent reason: Crime rate. This may interest you : Auto Insurance Market Still Has Room to Grow: AISUS, Allianz Partners, Progressive: Market Size, Sharing, Future Growth and Opportunity Assessment of Auto Insurance 2021-2027. Increased accidents, often caused by distracted drivers.

Why has my car insurance increased when nothing has changed? It’s also possible for your car insurance to go up without any changes to your driving history or policy. If your rates seem to have gone up for no reason, it could be because the company had to pay too many claims at once (like after a hurricane) or because things are generally more expensive.

What factors can increase your insurance rates?

Some factors that can affect your auto insurance premiums are your car, your driving habits, demographic factors, and the coverages, limits, and deductibles you choose. These factors can include things like your age, anti-theft features in your car, and your driving history.

What factors affect life insurance rates?

What factors are most important in determining your life insurance rates?

- Was. Age is one of the biggest factors that influence life insurance premiums. …

- Genre. …

- Height and weight. …

- Medical history. …

- Family history. …

- Smoking and Tobacco Use. …

- Occupation and Hobbies. …

- Lifestyle factors.

Traffic accidents and traffic violations are common explanations for increased insurance rates, but there are other reasons why car insurance premiums increase, including change of address, new vehicle, and claims in your zip code.

The accidents you cause almost always increase the price of insurance. Typically, insurers charge more for a fault accident. In certain states, however, your insurance company may not increase your premium for an accident if the damage is below a certain dollar amount.

Traffic accidents and traffic violations are common explanations for increased insurance rates, but there are other reasons why car insurance premiums increase, including change of address, new vehicle, and claims in your zip code.

Why would my car insurance go up for no reason?

Factors that affect car insurance rate increases can include things you can control, such as driving behavior, credit score, and place of residence. Other reasons car insurance goes up may be out of your control, such as your age, missing discounts, and number of claims in the area.

Can I ask my insurance to lower your rate?

Car insurance prices are non-negotiable, so you cannot ask your car insurance company to lower your rates. However, there are several ways to find more affordable prizes. Compare quotes from multiple insurers. Although states regulate the cost of car insurance, different companies offer varying rates.

How can I talk down my insurance rate?

Listed below are other things you can do to lower your insurance costs.

- Shop around. …

- Before buying a car, compare insurance costs. …

- Ask for higher deductibles. …

- Reduce coverage on older cars. …

- Buy your homeowner and auto coverage from the same insurance company. …

- Maintain a good credit history. …

- Take advantage of low mileage discounts.

Can I get a lower rate on my car insurance?

Keep a good driving record Not only do you avoid expensive speeding tickets or other traffic violation costs, but you also help keep insurance rates lower by proving that you are a less risky driver. Additionally, if you have a history free of claims or violations, you may receive additional discounts.

Can you negotiate with your insurance company?

Negotiation with the car insurance company. If the regulator’s initial offer is far below the estimates you’ve collected, you should negotiate with the insurer. You don’t need to file a lawsuit to get started. These discussions may take place in person or via email, but you must make the final decision in writing.

Is inflation causing car insurance to go up?

Like most other goods and services, inflation can also increase the cost of insurance.

Is car insurance going up with inflation? The average cost of full coverage car insurance will be $1,780 per year. The average cost of full coverage car insurance will be $1,780 per year.

Why is car insurance going up instead of down?

Inflation. Perhaps the biggest driver of higher car insurance premiums in 2022 is the same thing that is driving up costs across the board – inflation. Between June 2021 and June 2022, the Consumer Price Index (CPI) rose by 9.1%.

Why is car insurance going up in 2022?

Insurify says the main causes of the predicted increase are: “Americans are driving more, causing more total accidents; “Auto repair costs are rising, making every accident more expensive; âInflation is raising the costs of all goods and services; and.

While the price of gasoline, groceries and other essentials has skyrocketed in 2022, health care premiums for employer-sponsored coverage have remained roughly flat, according to a survey released Thursday.

Why does my insurance go up instead of down?

While it may seem arbitrary, there are real reasons why you might see your price go up and down. Car insurance rates can change based on factors like claims, driving history, adding new drivers to your policy, and even your credit score.

Why is car insurance increasing?

The number of car accidents has increased, leading to more insurance claims. This higher volume of claims, along with higher vehicle repair and replacement costs, is what is driving up insurance rates across the industry.

Why did insurance go up 2022?

If you’re wondering why your car insurance has gone up, you’re not alone. One of the most common reasons is simply because your insurer has raised your rates. Whether it’s to offset inflation, recover funds after a natural disaster, or cover higher claims, many insurers have raised rates in 2022.

Is car insurance increasing in 2022?

Insurify analyzed more than 69 million car policy rates and found that Americans paid an average of $1,777 for car insurance in 2022. This represents a 9% increase from 2021 and a 21% increase from 2020 Some states, including Oregon, Maryland and Virginia, saw average premiums rise by more than 25 percent.

Why is car insurance so expensive lately?

Common causes of overly expensive insurance rates include your age, driving record, credit history, coverage options, what car you drive and where you live. Anything that insurers can link to an increased likelihood of you having an accident and filing a claim will result in higher car insurance premiums.

Why do insurance rates keep increasing?

The number of car accidents has increased, leading to more insurance claims. This higher volume of claims, along with higher vehicle repair and replacement costs, is what is driving up insurance rates across the industry.

Why would my car insurance increase for no reason? Factors that affect car insurance rate increases can include things you can control, such as driving behavior, credit score, and place of residence. Other reasons car insurance goes up may be out of your control, such as your age, missing discounts, and number of claims in the area.

Why did insurance go up 2022?

If you’re wondering why your car insurance has gone up, you’re not alone. One of the most common reasons is simply because your insurer has raised your rates. Whether it’s to offset inflation, recover funds after a natural disaster, or cover higher claims, many insurers have raised rates in 2022.

While the price of gasoline, groceries and other essentials has skyrocketed in 2022, health care premiums for employer-sponsored coverage have remained roughly flat, according to a survey released Thursday.

Are insurance rates going up because of inflation?

Inflation has reached a 40-year high, and like almost everything else, car insurance rates are rising. Bankrate expects further increases in insurance rates to continue as insurers try to rebuild reserves while accident and repair costs remain high.

Why is car insurance going up in 2022?

Insurify says the main causes of the predicted increase are: “Americans are driving more, causing more total accidents; “Auto repair costs are rising, making every accident more expensive; âInflation is raising the costs of all goods and services; and.

Rising inflation, the changing nature of risk and a host of other economic factors are driving property insurance premiums higher than they have been in over a decade.

Employer-sponsored health insurance premium costs virtually unchanged in 2022. Annual family premiums for employer-sponsored health insurance average $22,463 this year, similar to last year ($22,221), according to research of 2022 KFF employer health benefits.

Why did my homeowners insurance go up so much?

There is no shortage of reasons for rising home insurance rates, but the likely culprits in 2023 are rising labor and construction costs due to inflation and costly natural disasters.

Insurify’s latest Auto Insurance Trends report predicts that the average annual auto insurance rate will increase an additional 7% to $1,895 in 2023, based on historical trends and the current state of the industry. In 2022, the national average cost of car insurance rose 9% to $1,777, according to the report.

Is homeowners insurance supposed to increase every year?

âIn most cases, your home insurance premium will increase each year. Premiums often increase to keep up with inflation and the age of your home. If you’ve submitted a claim against your policy, this could also affect your insurance score and homeowner’s insurance premium.

Why does my house insurance keep going up?

Skyrocketing inflation is one of the main culprits behind rising premiums. Home insurance coverage is based on the cost to rebuild your home, and this may have gone up dramatically as the price of many building materials has increased and supply chain issues have made the construction process more expensive.

Can I freeze my car insurance?

Should I maintain car insurance if I don’t have a car? If you don’t own a car, you’ll still need auto insurance if you want to drive while traveling, for example, or if you want to avoid your future rates going up due to a lapse in coverage. For these circumstances and others, a type of coverage called “non-owner” car insurance may be a good idea.

Can you freeze insure?

Technically, you can’t “pause” or “freeze” your auto insurance – it’s required by law in almost every state. The only way to pause your car insurance is to cancel your coverage entirely, which you should only do when changing policies or disposing of your car.

Can I pause my insurance Geico?

GEICO does not provide the ability to suspend coverage. However, if you cannot afford car insurance, call GEICO directly at 1-800-207-7847 to discuss other options.

Can I cancel my insurance policy and get my money back?

If you choose to cancel your policy or your insurance company cancels it, you will normally not receive a car insurance refund unless you have paid the premium in advance.

Is it possible to pause your car insurance?

Depending on your state’s rules, you may be able to pause your car insurance if you won’t be driving for an extended period of time. You might consider suspending your car insurance if you are: Taking a long trip and not driving. Go to college and not drive.

Can I pause my car insurance nationwide?

There’s no legal way to freeze your car insurance policy if you’re still driving, but you can cancel your coverage indefinitely if you’re away for an extended period of time.

What is insurance freeze?

One of the ways to keep your life insurance premiums affordable, if available by your insurer, is the premium freeze option. It allows you to freeze your premiums, which you might want to consider if they are becoming too expensive or unaffordable.

Is freezing covered in an auto policy?

Typically, collision and comprehensive coverage exclusions include loss or damage due to: Wear and tear. Freezing. Mechanical or electrical breakdown or failure.

Do you need to unfreeze credit for car insurance?

It is not necessary. If you want to add an insurance policy or switch an existing policy, unfreeze your credit for a brief period of time to allow insurers to access your credit history or credit score.

What happens if you pause your car insurance?

The vehicle will not be covered if someone wants to drive it. The vehicle will not be insured against non-driving issues such as fire, damage to animals, vandalism or theft. You will have a coverage lapse, which can increase your future rates.