Don’t Drive Your Car Much? Pay Per Mile Car Insurance Could Save You Big Money

If you want to reduce the cost of your car insurance and you don’t drive a lot with your car, you can consider switching to car insurance where you pay per kilometer. Instead of paying an exact amount for your auto insurance each month, pay-per-mile insurance allows you to pay a lower flat rate plus cash for every mile you drive.

The concept of pay-per-mile auto insurance has been around since 1968 and can help some motorists save money. In 2008, the Brookings Institute found that insurance per mile would save society “$50 to 60 billion a year by reducing traffic-related damage.”

Not only can car insurance based on auto insurance cost you less money, it can also give you more control over how much you drive and spend on gas. The advantage is also that you know the exact cost of every kilometer you drive. According to Robert Lajdziak of J.D. Power are “even customers who don’t save money are still more satisfied with the price because of greater transparency and a sense of control over their premiums.”

Learn how pay-per-mile auto insurance works, which auto insurance providers offer coverage, how much money you can save, and whether pay-per-mile auto insurance might be right for you. Find out more about our top picks for the cheapest car insurance.

What is pay-per-mile car insurance?

Contents

- 1 What is pay-per-mile car insurance?

- 2 How does pay-per-mile car insurance work?

- 3 Who sells pay-per-mile car insurance?

- 4 Who can get pay-per-mile car insurance?

- 5 How much does pay-per mile car insurance cost?

- 6 What is the most expensive part of owning a car?

- 7 How can insurance save you money?

- 8 What happens if you go over your annual mileage on finance?

- 9 How long will a car with 150k miles last?

Pay-per-mile auto insurance charges you monthly based on how much you drive. See the article : Sedan vs. Coupe: Which is the cheapest car to insure?. Instead of paying a fixed premium for your car insurance, you pay a variable amount that fluctuates depending on how many miles you put on your car.

How does pay-per-mile car insurance work?

You pay your auto insurance company a standard base rate, plus a rate per mile that is multiplied by the number of miles you drive each month. On the same subject : How auto insurance claims are deposited.

To keep track of mileage, most pay-by-mile auto insurance companies require you to plug an electronic device into your car’s OBD (onboard diagnostic) port. Also known as telematics devices, these machines can also monitor other driving behaviour, such as driving speed, acceleration and braking distance.

If you don’t want your auto insurance company to track your driving, some companies let you track your mileage through smartphone apps or odometer photos.

Who sells pay-per-mile car insurance?

Currently, four auto insurers offer pay as you go insurance: Allstate, Metromile, Mile Auto and Nationwide. This may interest you : General Car Insurance Explained – Forbes Advisor UK.

Metromile and Mile Auto are both online-only insurance providers that only offer auto insurance. Allstate and Nationwide are larger, traditional insurance companies that sell many types of insurance, allowing further potential savings from bundling home, life, or other insurance policies.

For military personnel and families, it’s worth mentioning the “pay as you drive” auto insurance program offered by USAA subsidiary Noblr. The “Ubi Program” (Usage-based Insurance) will lower your bill when you drive less, but the algorithm for calculating your monthly premium isn’t exactly tied to your mileage, so technically it’s not insurance per mile.

Who can get pay-per-mile car insurance?

Pay-as-you-go auto insurance exists in most of the 50 US states except Alaska, Hawaii, Louisiana, New York, and North Carolina. Account requirements vary between insurers.

The largest coverage comes from Nationwide SmartMiles, which offers policies to all but the five listed above. Smaller, online-only insurance companies only offer auto insurance policies in eight or nine states.

How much does pay-per mile car insurance cost?

Car insurance rates per mile vary depending on a number of factors. Your personal monthly premium will depend on your age, your gender, your location, the type of car you drive, other drivers of the vehicle and your driving history – especially recent speeding, negligence, or drink-driving accidents.

Compare the auto insurance companies and plans that pay per mile below to learn more about how they work and some estimated prices for common scenarios.

Note: All insurance quotes provided are only estimates of potential car insurance costs per mile. The final cost of actual insurance policies may differ significantly from these estimates.

The auto insurance quotes below are based on my own personal driving situation — two record-breaking drivers about 50 years old living in Berkeley, California, with one car — a 2008 Subaru Outback. My standard quote was $15,000 each. person ($30,000 per incident) coverage for personal injury, $5,000 for property damage, $15,000 per person ($30,000 per incident) for injuries caused by uninsured or underinsured motorists, and comprehensive and collision coverage with $500 deductible for each.

Metromile

Founded in California in 2011, Metromile was one of the first pay-per-mile auto insurance providers. To track mileage, Metromile uses a device called the Pulse that connects through your OBD port.

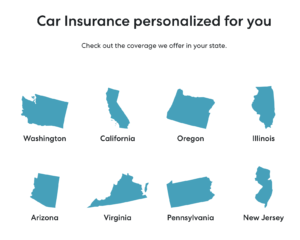

Metromile has a fairly small footprint to date, offering insurance policies in eight states: Arizona, California, Illinois, New Jersey, Oregon, Pennsylvania, Virginia, and Washington.

With Metromile, for every mile you drive, you pay up to 250 per day (150 per day for New Jersey). Metromil claims its customers “save an average of 47% compared to what they paid to their previous auto insurer.”

Based on my location and driving situation, Metromile’s online system gave me a base rate of $33 per month plus 6 cents per mile. At a driving speed of 500 miles per month, or 6000 miles per year, I would pay $63 each month for auto insurance, or $756 per year. That’s for the pretty standard insurance coverage mentioned above.

At a lower level of coverage, no-collision, comprehensive, or uninsured motorist coverage, Metromile quoted me as a base rate of $20 per month and 3 cents per mile. If I drive 500 miles a month, I’ll pay $35 a month or $420 a year.

Metromile was acquired by insurance company Lemonade in November 2021. It’s still unclear if and how Metromile will combine with Lemonade’s homeowners, renters and pet insurance products.

Mile Auto

Mile Auto – or simply Mile, as the company calls itself – is unique in the per-mile insurance industry because you don’t need to install anything that tracks your car’s usage and driving.

Instead, Mile uses a smartphone app that allows you to submit photos of your car’s odometer. Called MVerity, the app will send you a monthly reminder with a link that will open your phone camera. Attach your odometer, upload your photo and MVerity will do the rest. It detects your odometer data by confirming your vehicle and the authenticity of the photo, then comparing your photo with previous mileage.

Also unique to Mile Auto is the lack of a daily mileage limit. You pay for all your kilometers driven, even on long journeys. Mile Auto is available in nine states: Arizona, California, Georgia, Illinois, Ohio, Oregon, Pennsylvania, Tennessee and Texas.

Based on a quote for location and driving situation, Mile Auto estimated a base rate of $38.03 per month and a per-mile fee of 4.2 cents per mile, for the same standard collision, extended and uninsured motorist coverage parameters that I have for Metromile used. At 500 miles a month, that would also cost me about $59 a month or $708 a year.

At minimal coverage (with the same minimal personal injury coverage as Metromile), Mile Auto offered me no savings. It quoted me a base rate of $34.68 and a rate per mile of 4.9 cents. At 500 miles a month, I’d still pay $59 a month, or $708 a year. Mile Auto has not yet responded to requests for comment.

Nationwide SmartMiles

Like Metromile, Nationwide SmartMiles works by plugging a small device that tracks your mileage and driving into your car’s OBD port. Like most other programs, SmartMiles limits your maximum daily mileage to 250.

Nationwide SmartMiles is available in 45 states and Washington, DC — every state except Alaska, Hawaii, Louisiana, New York, and North Carolina.

This program doesn’t offer a simple online quote system – you can get a quote for traditional auto insurance, but nothing that explicitly gives a monthly base rate or cost per mile.

After a few minutes with a Nationwide representative, I was able to get a quote for coverage similar to the general insurance scenario described above for Metromile and Mile Auto.

Nationwide estimated I would pay about $65 a month with my 500 mile estimate. The rep said the rate per mile would be 5 cents, making the monthly base rate $40. Remember, that’s for $15,000/$30,000 Basic Personal Injury Coverage, $500 Collision Deductible and Comprehensive Coverage, $5,000 Property Damage and $15,000/$30,000 for Uninsured Motorist Coverage.

Allstate Milewise

Milewise is one of two telematics programs from Allstate — the other is Drivewise, a traditional insurance policy that offers safe driving discounts for those who want to install a monitoring device on their car’s OBD ports.

Allstate Milewise is available in 21 states — Arizona, Delaware, Florida, Idaho, Illinois, Indiana, Maryland, Massachusetts, Minnesota, Missouri, New Jersey, Ohio, Oklahoma, Oregon, Pennsylvania, South Carolina, Texas, Virginia, Washington, West Virginia and Wisconsin — as well as Washington, DC.

Drivers in most states have a maximum of 250 miles per day, although in Illinois, Indiana, New Jersey, Ohio and Oregon it is capped at 240 miles.

Allstate Milewise is not available in California so I was unable to get an actual quote for my particular driver situation. An Allstate representative told me that “With Milewise, low mileage drivers can typically save 50% over traditional insurance policies.”

Because rates vary so widely based on individual drivers and the amount of insurance coverage, I recommend taking the time to fill out the online quote tools or call the companies to get insurance quotes based on your own specific driving situation.

To learn more, check out our best cheap auto insurance companies and seven more ways to save money on auto insurance.

The editorial content on this page is based solely on objective, independent reviews by our writers and is not influenced by advertising or partnerships. It is not provided or commissioned by any third party. However, we may receive compensation when you click on links to products or services from our partners.

What is the most expensive part of owning a car?

The six most important costs of owning a car

- Fuel. The average cost is $1,681.50, or 11.2 cents per mile. …

- Financing charges. …

- depreciation. …

- Insurance. …

- Maintenance and tires. …

- Licenses, Registration and Taxes.

Which part is the most expensive in a car? The engine The most expensive part to repair is the car engine. Car engine replacement can cost upwards of $10,000 in a small car and even more in a truck or SUV.

What costs go into owning a car?

For vehicles traveling 15,000 miles per year, the average cost of car ownership in 2022 was $10,728 per year, or $894 per month, according to AAA. That figure includes depreciation, interest on loans, fuel, insurance, maintenance and fees.

What are five factors that affect the operating costs of a vehicle?

Factors influencing vehicle operating costs include vehicle type, vehicle speed, changes in speed, slope and road surface [21, 22].

How can insurance save you money?

Look at the impact of higher deductibles You can save money by increasing the deductible on your comprehensive and collision coverage. The deductible is the amount that the insurer will not cover for repairs – this is the amount for which you are responsible. If you don’t have an accident, you will save extra money.

How can buying insurance help you? Insurance is a way to manage your risk. When you buy insurance, you buy protection against unexpected financial losses. The insurance company will pay you or someone you choose if something bad happens to you. If you are not insured and an accident occurs, you may be responsible for all related costs.

Can health insurance save you money?

Health insurance helps you save money because you can transfer a large financial risk to the insurer for a (relatively) small premium. I’m not saying health insurance isn’t expensive. The cost of health insurance has been rising faster than headline inflation and workers’ wages for years.

Why do people avoid buying health insurance?

you have unexpected expenses for a sick, disabled or aging family member. your income is too low to file a tax return. the lowest-priced coverage available, through a Marketplace or a job-based plan, would cost more than 8.05 percent of your household income.

Is it worth it to not have health insurance?

Without health insurance, a serious accident or health problem resulting in emergency care and/or an expensive treatment plan can result in poor creditworthiness or even bankruptcy.

Why is health insurance a good idea?

Health insurance protects you against unexpected, high medical costs. You pay less for covered care within the network, even before you meet your deductible. You get free preventive care, such as vaccines, screenings, and some checkups, even before you reach your deductible.

What happens if you go over your annual mileage on finance?

Over-mileage costs are the fees you pay to the financier if you exceed your pre-agreed mileage allowance. The additional mileage allowance is calculated at a rate of pence per mile. Simply put, the more you go over your pre-agreed mileage, the more it will cost you in extra mileage.

Can you negotiate too high a mileage with a lease? Some leases allow 15,000 miles, but more manufacturers reduce the fee to just 10,000 or 12,000 miles per year. If you think you are likely to exceed the limit, negotiate additional mileage in advance. This can save you a few cents per kilometer on the mileage allowance at the end of the lease.

How can I avoid paying excess mileage?

If you buy out your car lease, you do not have to pay an extra mileage allowance, because you buy the lease car at the residual value or the amount that your leasing company expected the car to be worth at the end of the lease. In that case, you keep your car and avoid mileage reimbursement.

How can I get out of paying excess mileage?

One of the best ways to escape the over-limit fee is to negotiate a lease repurchase at the end of the term, if your budget allows. If you turn in your car and find yourself owed thousands of dollars in additional mileage fees, it’s better to use that as a down payment for the vehicle.

What happens if you exceed lease mileage?

Excess Mileage Most leasing companies charge about 15 to 20 cents per mile above the amount allowed in the contract, usually 12,000 miles per year. If you go way over the allowed mileage and you’re looking at a big fine, you still have options. If you like the car, you can buy it instead of paying the mileage allowance.

What happens if you go over your mileage?

If you put more miles on it, it could cost you a pretty penny. Many leasing companies charge around $0.15 to $0.30 per additional mile. That doesn’t seem like much, but it can add up quickly. If you drive more than 1,000 miles, it could potentially cost you about $150 to $300 when you return the vehicle to the dealer.

How much does Honda charge for mileage overage?

It is important to know and adhere to your lease mileage limit. If you pass, you will be charged extra per kilometer; for Honda leases, this mileage penalty is typically between $0.15-$0.20 per mile. For example, if you turn in your lease with 1,000 miles over the limit, you’ll be fined $200.

Can you go over your mileage?

Insurers often use annual mileage to calculate the price of your auto insurance, so it’s important to be as accurate as possible. Exceeding your annual mileage well can void your auto insurance policy.

How many miles can I go over my lease?

It is common for lease contracts to have an annual mileage limit of 10,000, 12,000 or 15,000 miles. If you exceed this mileage limit, you may be charged up to 30 cents per additional mile at the end of the lease term.

What happens if you go over the miles on your lease?

Excess Mileage Most leasing companies charge about 15 to 20 cents per mile above the amount allowed in the contract, usually 12,000 miles per year. If you go way over the allowed mileage and you’re looking at a big fine, you still have options. If you like the car, you can buy it instead of paying the mileage allowance.

Can I buy more miles for my lease?

No. You cannot buy additional lease miles during a lease, only at the beginning. If you are already in a rental contract and you see that you are already exceeding your allowance, there are a number of options. See our article, Vehicle Lease on Mileage for more details.

How long will a car with 150k miles last?

| Age of the vehicle in years | Average mileage |

|---|---|

| 15 | 180,000 |

Can a car drive up to 400,000 miles? THERE is no secret to letting your car live to a ripe old mileage. Luck might get you there, but it’s no surprise that many vehicles that have reached 200,000, 400,000 and even 500,000 miles have been given extraordinary care and maintenance, often with the owners doing the routine work themselves.

What mileage is too high for a used car?

What is considered high mileage on a car? Often, 100,000 miles is considered a cut-off point for used cars, as older vehicles often require more expensive and frequent maintenance when the mileage exceeds 100,000.

Is it OK to buy a used car with high mileage?

It can be somewhat risky to buy a vehicle that has traveled more than 100,000 miles. Even if it is well maintained and has about 100,000 miles on the clock, such a car is already past its prime. In general, vehicles are likely to start experiencing problems after 100,000 miles.

How long will a car with 120k miles last?

Mileage varies between vehicles, but a good rule of thumb is that people drive about 12,000 miles a year on average. Therefore, 120,000 miles would be a good mileage for a used car about 10 years old.

Is 200000 miles alot for a car?

There is no absolute mileage that is too much for a used car. But consider 200,000 an upper limit, a threshold at which even modern cars begin to succumb to the years of wear and tear.

Can car last 200 000 miles?

A conventional car can last 200,000 kilometers. Some well-maintained car models reach a total of 300,000 or more miles. The average age of passenger cars is currently around 12 years in the United States. By choosing a well-built make and model, you can extend the life of your car.

How long will a car last after 200 000 miles?

In general, most modern cars can go 200,000 miles without major problems, provided the vehicle is properly maintained. Considering that an average person drives 10,000-20,000 miles per year, this equates to about 15 years of service.